Last Week in Review: Less Equals More for Rates

This past week long-term interest rates fell to their lowest levels since mid-February. Let us go through some reasons why rates declined and what it means for the second half of 2021.

From More to Less

The great reopening of the U.S. economy appears to be fizzling. There are still 9.3M open jobs available, which means the labor market is improving, but slowly. The effect of fewer employed means there will be softening economic growth and lower inflation. Bonds love low inflation, and seeing the 10-year note yield hit 1.25% this past week suggests that higher inflation will indeed be transitory.

Another thing we are getting less of is policy response, both from Congress and the Fed. On the former, the original proposal from the White House was another $4 trillion in economic stimulus through the American Infrastructure Plan and American Families Plan. Those proposals are being batted around Congress and will likely end up being a fraction of the original proposal.

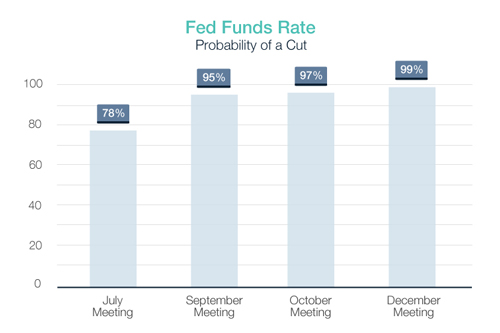

On the latter, the Federal Reserve, who has been so accommodative during COVID, will be less so going forward. At the recent Fed meeting, they changed their forecast from initially hiking rates in 2024 to hiking as many as three times in 2023.

And on the bond-buying program, where the Fed has been purchasing at least $40 billion worth of mortgage bonds each month, they will be doing less in the future, and the pressure is on to start tapering. At the last Fed meeting, some Fed members cited a scorching hot housing market as a reason to stop buying mortgage-backed securities.

Return of Familiar Tailwinds

US bond yields are relatively attractive compared to other large bond markets around the globe like Germany and Japan where their 10-year yields are -0.31% and 0.02%, respectively. This helps the U.S. attract investments from around the globe, thereby pushing yields lower.

Bottom line: Markets tend to overshoot to both the upside and downside, meaning this revisit to rates in February could be fleeting. For anyone considering a mortgage, now is the time.